October 17, 2018

Say “YES” to Express!

The most common question our underwriters are asked after offering an applicant one of our Express Standard classes is, “What does Express mean?”

If you aren’t familiar with the Express classes we offer, you may not be quoting your client properly and could potentially be missing an opportunity for quick policy issue.

Many of our products at amounts $250,000 and below, offer Express Standard1, Express Standard2 and Express Standard Tobacco. The advantage of having Express classes is that it allows underwriters to categorize risks much easier, especially when an applicant has mild impairments or is overweight. Express classes also utilize quick, streamlined underwriting which means fewer requirements for you and your client to satisfy! For example, it could mean obtaining a questionnaire over securing medical records or exam & labs.

National Life defines the Express classes as follows:

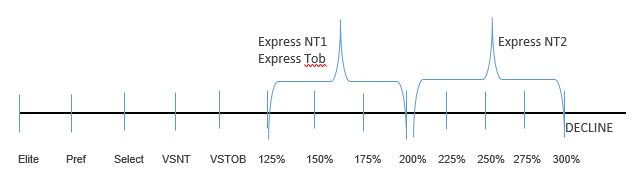

Express Standard Non-Tobacco1: Available to applicants who do not use tobacco or nicotine products and who are assessed by underwriting with a rating equivalent 150% to 200% (two to four tables). Living Benefits are available unless client doesn’t qualify for cause.

Express Standard Non-Tobacco2: Available to applicants who do not use tobacco or nicotine products and who are assessed by underwriting with rating equivalent of 225% to 300% (five to eight tables). Living Benefit riders are not available on ESNT2.

Express Standard Tobacco: Available to tobacco and nicotine users who are assessed with a rating equivalent of 150% to 200% (two to four tables). We do not currently offer an Express Tobacco class for risks beyond 200%.

To illustrate:

Anyone assessed at higher than Standard mortality is considered substandard (or rated). Mildly substandard risks that fit nicely into our Express Non-tobacco1 class are:

• Well controlled, non-nicotine type 2 diabetics treated 2 oral medications or less

• Overweight applicants with a BMI of > 38

• A single impairment that requires more than one medication to control (i.e. anxiety, depression, high blood pressure, arthritis, asthma, inflammatory bowel).

• Clients with unfavorable factors that would generate a low risk classifier score.

*CLICK HERE for more information on our EZ Underwriting Checklist distinguishing between favorable and unfavorable responses.

And as always, if you’re unsure how to quote your client, we recommend sending a quick quote to underwritingquotes@nationallife.com so we can assist you before taking an application.

So next time you’re quoting a client who’s not a standard risk, say “Yes” to Express!

Felicia McElhaney

AVP Underwriting, Business Acquisition

TC104525(1018)1